UNIDO Manufacturing Sector Technical Note _ July 2020

By Tichaona Mushayandebvu (UNIDO Country Representative – Zimbabwe)

Section 1: Overview

Manufacturing – a key driver of economic growth and structural transformation

There is overwhelming global consensus that industrialization plays a pivotal role in a nation’s economic growth and competitiveness. Pursuing systematic and sustained industrialization has long lasting benefits on economic development as confirmed by history of industrialization in Europe, North America and Asia. Kaldor’s law provides a conceptual framework for the link between manufacturing and economic growth. “Manufacturing sector displays levels of productivity that are higher compared to those of other sectors and has a greater capacity to absorb labour force. It also promotes savings, boosts the process of capital accumulation and offers higher investment opportunities. In addition, Engels law states that demand for manufacturing products increases as the economy grows and a country gets richer. “Not only the absolute amount spent on manufacturing, but the proportion of share of your income spent on manufacturing increase.

Context

The analysis of the performance of Zimbabwe Industry (herein referred to as the manufacturing[i] sector) is based on UNIDO’s Country and Industry profile methodology which uses five group indicators reflecting the (i) Scale and intensity of Manufacturing activities, (ii) Inclusiveness within the manufacturing sector, (iii) Sustainability of the Manufacturing sector, (iv ) Technological capabilities and innovation and (v) Subsector level analysis. Subsector level analysis has two components namely diversification & specialization and subsectors competitiveness. In addition, Zimbabwe’s Industry performance is benchmarked with four competitors, selected members of SADC and COMESA, namely Zambia, Tanzania, Kenya and Egypt and South Africa. All figures used in this section are based on UNIDO SDG 9 indicators. During the past 30 years, the manufacturing sector in Zimbabwe has gone through a major structural transformation. These changes require further analytical work so as to identify the most affected subsectors underpinning de-industrialisation and inform future strategy and policy making processes.

According to UNIDO’s Department of Policy Research and Statistics (PRS), it is too early to have statistical evidence to show the impact of COVID 19 pandemic on industry. However, anecdotal evidence and opinion pieces seem to suggest that COVID 19 pandemic has the potential to have adverse effect on Industries worldwide, especially for smaller enterprises and in less developed regions of the world. In response to COVID 19 pandemic, many firms have started to promote digitalisation of their labour activities and production processes, while other global manufacturers have started to consider introducing more flexibility in their business models, e.g. with regard to their product lines, sources of inputs, people and skills[ii], while others are looking to source inputs from less distant suppliers and to re-shore their production[iii].

In addition new production related concepts such as ‘just in case’ alongside the popular ‘just in time’ and ‘near shoring’ alongside ‘reshoring’ have emerged. These developments will have serious consequences for developing countries as they become increasingly excluded from participating in Global Value Chains (GVCs).

Unpublished results of UNIDO’s Africa wide rapid survey carried out early in June is expected to confirm that the pandemic and its ‘shutdowns’ of March to May 2020 negatively impacted on the manufacturing sector. This rapid survey targeted Ministries of Industry and Commerce in all 54 African countries. The survey results for Zimbabwe show that the most affected manufacturing subsectors were the Food & Beverages and the Plastics, Packaging & Printing subsectors. The Clothing & Textiles[iv] subsector recorded minimal gains due to increased demand for work suits, facemasks and bed sheets for hospitals. Challenges experienced by the manufacturing sector included shortages of raw-materials and inputs sourced locally or externally depending on their technological complexities. In addition, effective demand for goods and services also declined on the back of travel restrictions and shorter working-hour regimes.

Section 2: Manufacturing Analysis

The performance of Zimbabwe’s Manufacturing sector is best shown when it is analysed in relationship with regional counterparts in SADC/COMESA namely Zambia, Tanzania, Kenya and Egypt and South Africa.

Scale and intensity of manufacturing activities

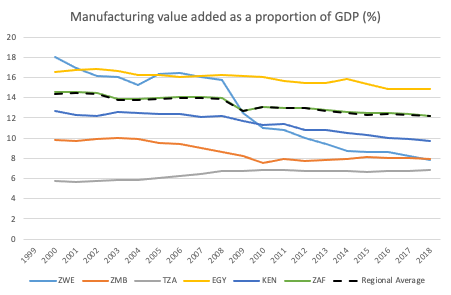

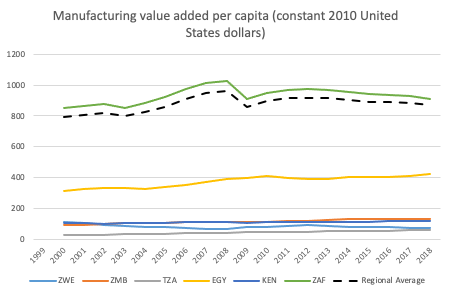

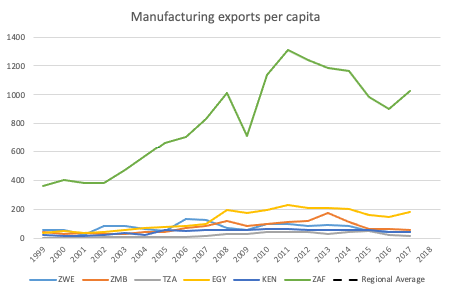

Both the share of MVA[v] in GDP and per capita MVA can be used to compare the manufacturing sector’s significance role in different countries. The two indicators are important measures to analyse growth enhancing structural[vi] change in the economy. MVA as a share of GDP and per capita MVA are calculated by dividing the manufacturing sector’s total value added in a given year by the total GDP and population size, respectively.

Figure 1: Manufacturing value added as a proportion of GDP

Source: UNIDO SDG Indicators

Figure 2: Manufacturing value added per capita (constant 2020 United States dollars)

Source: UNIDO SDG Indicators

Figure 3: Manufacturing exports per capita

Source: UNIDO CIP index

All the three indicators MVA/GDP, MVA/capita and Manufacturing exports/capita should be interpreted together as a proxy for the strength of the country’s manufacturing sector. Generally, the stronger the country’s performance in all three indicators[vii], the more successful is its manufacturing sector. The development of the Zimbabwe’s National Development Strategy 2021 -2025 offers a great opportunity for recovery, growth and enhancing competitiveness of Zimbabwe’s manufacturing sector and selected key subsectors.

Inclusiveness within manufacturing

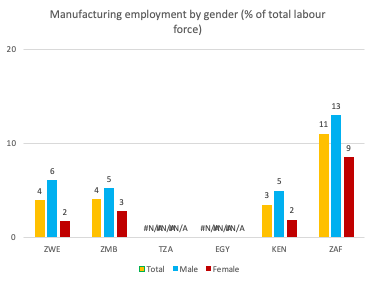

Industrialization is only beneficial to the society when it creates employment opportunities in the formal economy. This is captured by the SDG indicator on manufacturing employment[viii] based on the share of manufacturing employment in total employment. This indicator also measures Inclusiveness in manufacturing employment disaggregated by gender. Figure 4, show that manufacturing sector employment in Zimbabwe is at 4% of total employment. However, this compares well with its comparators such as Zambia and Kenya at 4% and 3% respectively. Employment of women is still a challenge in Zimbabwe and the Africa region and there is need for more work in ensuring gender parity and inclusiveness. Gender mainstreaming is a key hallmark of Inclusive and Sustainable Industrial Development.

Figure 4: Manufacturing Employment by Gender (% of total labour force)

Source: ILO

Sustainability of the Manufacturing sector

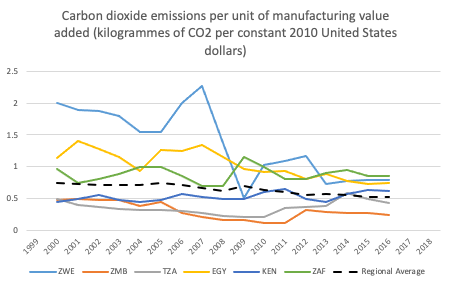

A country’s economy must not grow at the expense of its natural environment, a valuable asset of the country’s industrial sector and above all, the long-term welfare of its current and future generations. To achieve Inclusive and Sustainable Industrial Development (ISID), therefore, focusing on the promotion of inclusiveness alone is not sufficient. Instead, the country must introduce specific measures to make manufacturing production cleaner, greener and more circular. In line with SDG indicators, a country’s emission intensity[ix] (kgCO2 per unit of MVA) is a proxy for its manufacturing sector’s sustainability.

Figure 5, shows that Zimbabwe’s emission intensity (carbon dioxide emission per unit of manufacturing value added in kgCO2) of 2kgCO2 in 2000 increased to 2.27kgCO2 in 2007. This emission intensity was above that of its comparators which averaged below 0.65 kgCO2 during the period under review. Closer to Zimbabwe’s performance was Egypt which had an emission intensity of 1.30kgCO2.

Zimbabwe’s emission intensity reduced from a high of 2.27kgCO2 in 2007 to a low of 0.51kgCO2 in 2009. With this average, Zimbabwe’s emission compares reasonably well with those of Egypt at 0.79kgCO2 and South Africa of 0.87kgCO2. Working papers developed under the auspices of Zimbabwe’s National Determined Contribution (NDC) exercise of UNFCCC processes indicate that in 2017, Energy production (coal based) contributed 57% of the total CO2 emissions, followed by ferroalloys and cement production at 22.7% and 19.8% respectively.

Figure 5: Carbon Dioxide Emissions per unit of manufacturing value added

Source: UNIDO SDG indicators

Technological capabilities and innovation

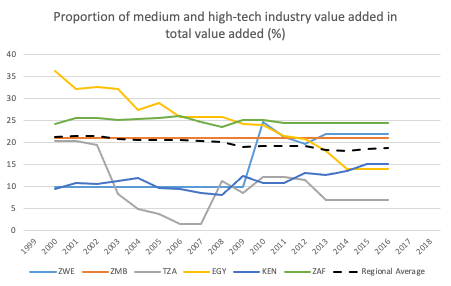

Growth enhancing and competitive structural change does not only entail moving away from agriculture[x] to manufacturing but can also occur within the manufacturing sector itself. It is generally accepted that by enhancing technology content of activities and progressively shifting from low- to medium and high-tech industries, greater value addition will take place in the economy.

Figure 6, shows that in 2000 Zimbabwe’s proportion of medium and high-tech industry value added in total value added (MHT indicator in %) stood at 9.9% compared to its comparators average of 26.07% (excluding Kenya whose MHT indicator was 9.5% from 2005). Zimbabwe maintained that status quo up-to 2009 with Tanzania being the only comparator country having its MHT indicator at 8.56%. In 2010, Zimbabwe’s MHT indicator more than doubled to 24.65% and outpaced all its comparator countries though lower than South Africa MHT indicator level of 25.16%. The MHT indicator slightly decreased thereafter to end 2016 at 21.82% and above all its comparators but lower than South Africa. The upsurge of MHT indicator Zimbabwe experienced post 2009 require further subsector analysis to understand the characteristics and trends of both the MHT and Low tech investments[xi] undertaken in Zimbabwe.

Figure 15: Proportion of medium high-tech industry value added in total value added

Source: UNIDO SDG Indicators

Section 3: Within Manufacturing Analysis on industry sub-sector level

To further understand and appreciate the performance of the manufacturing sector, it is necessary to analyse the structure of the manufacturing sector itself as well as the competiveness of the different sub-sectors. To analyse the size and performance of different subsectors, we make use of the International Standard Classification of all Economic Activities (ISIC) within the sector D which covers classification 15 (Food and beverages) to 37 (Recycling).

Diversification and specialisation

While diversification is generally considered desirable, specialization and higher manufacturing value added based on fewer industries can lead to higher value retention or earnings in country than lower manufacturing value added derived from a larger number of industries. Thus, diversification itself should not be the goal of manufacturing development but could be considered a means to achieving the upgrade of the manufacturing sector’s industrial structure to secure sustained growth of manufacturing value added and higher levels of technological and innovation capabilities. In addition, as a country seeks to grow or expand its industrial base, it should also pay attention to whether it has adequate capacities and capabilities to sustain such growth.

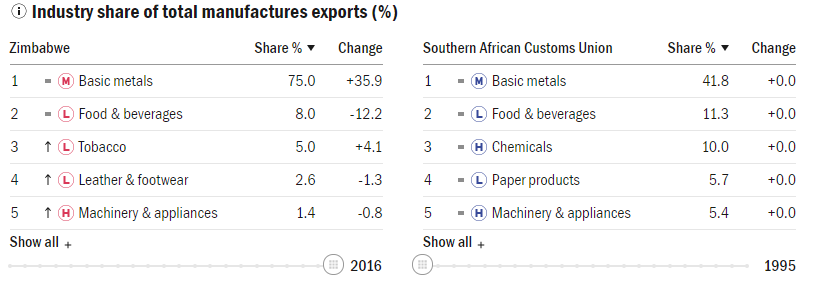

Table 1, shows that Basic Metal production (medium tech) dominates the percentage share of total manufactured exports of Zimbabwe. Basic metal share stood at 75%, followed by Food and Beverages (low tech) at 8.0% and Tobacco (low tech) at 5.0%.

Table 1: Industry share of total manufactures exports (%)

Source: IAP.UNIDO.ORG

Competiveness of the manufacturing sub-sectors

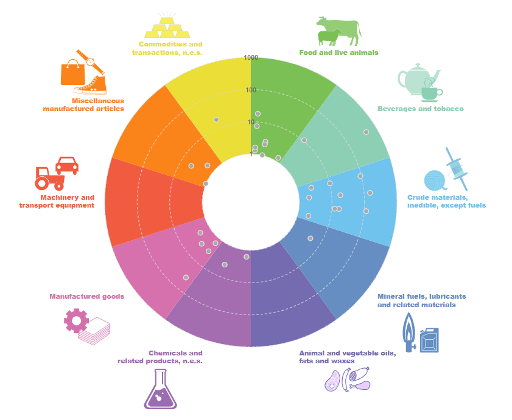

Industrial competitiveness is a key determinant of economic growth and also contributes to poverty reduction. Industrial competiveness is affected by several factors including those affecting export competitiveness which we have already analysed earlier on in this Manufacturing Sector Note. The capacity to export is an important dimension when analysing a country’s economic growth and competitiveness. A concept that is of particular interest for this analysis is a country’s Revealed Comparative Advantage (RCA).[xii]

Radar Plot 1: Revealed Competitive Advantage

Source: UNCTADSTA

The above RCA radar plot shows that Zimbabwe has 5 products classified as ‘Manufactured goods’, 2 products under the ‘Chemical and related products’ and 3 under the ‘Miscellaneous manufactured articles’. Under these three manufacturing categories, ‘Pig iron and spiegeleisen’ valued at $327 450k leads with an RCA of 37.8 whilst ‘Printed matter’ (valued at $41 040k) is second and followed by ‘Dyeing and Tanning extracts’ (valued at $2 027k) with RCAs of 4.5 and 4.0, respectively.

In terms of number of products with an RCAS above 1, Zimbabwe’s exports are dominated by the ‘Crude materials, inedible, except fuels’ and the ‘Food and live animals’ sectors which have a total of 10 and 8 products, respectively. In terms of level of RCA, ‘Tobacco, unmanufactured, tobacco refuse’ under the ‘Beverages and Tobacco” sector dominates at RCA of 465.5 and with export value of $1,161m in 2018. In terms of export value earned, the ‘Gold, no monetary excluding ores and concentrates’ under the ‘Commodities and transactions’ sector dominates at $1,236m in 2018 and with an RCA of 18.7.

The above shows that Zimbabwe’s manufacturing sector may have to ‘move up the value chain’[xiii] as an industrial competiveness strategy and produce more medium to High tech products in the ‘Crude materials and inedible’, ‘Food and live animals’, ‘Beverages and Tobacco’ and ‘Commodities and transactions’ subsectors. In addition, the number of manufactured products with an RCA greater than 1 (one) may need to be increased from the current total of 10 by a targeted factor established in the framework of revised ZNIDP and or the NDS TWG 5. In particular, Tobacco and Gold which has both outstanding RCAs and export volume offer the best opportunities upon which value addition based manufacturing could reap huge rewards and impact for Zimbabwe’s industrialization and structural transformation agenda.

Section 4. Potential Outcomes – recommendations

The analysis provides a ‘bird’s view’ of the performance of industry. It introduces objective and globally accepted indicators which potentially could be used to measure outcome and outputs of the proposed Thematic Result 5 “Moving the economy up the Value Chain and Structural Transformation” of the NDS 2021 -2025. To suggest some outcome and outputs for Thematic Result 5, I am proposing a couple of assumptions based on Zimbabwe’s broad vision to attain the ‘upper middle income’[xiv] status by 2030 with a minimum GNI (GDP per Capita) US$4,000. Assuming that Zimbabwe target GDP per Capita for 2030 is at US$4,000, given its current capacities and capabilities, it is possible to increase its current GDP per Capita of US$1,200 to US$2,000 by end of 2025 and subsequently doubling the same to meet its 2030 target. Zimbabwe’s a current MVA/GDP is 8% i.e. US$96 per capita. I am also assuming that MVA/GDP ratio target will increase to 10%, i.e. US$200 per capita by end of 2025. It is my view that suggested key interventions or activities listed below, if adequately resourced and systematically implemented, could support recovery, structural transformation and growth on the manufacturing sector. The interventions could also enhance competitiveness of the manufacturing sector in Zimbabwe and potentially double MVA/GDP rate to between 18-20% by 2030.

The NDS and Vision 2030 Agenda should directly reflect the urgent need to bolster the manufacturing sector, structurally transform the sector, introduce opportunities for growth in selected key value chains and put in place capacities and capabilities to enhance manufacturing sector competitiveness, i.e. it is about the broad Inclusive and Sustainable Industrial Development agenda for Recovery, Growth and Competitiveness. In short, Thematic Result 5 of the NDS could be ISID for Recovery, Growth and Competitiveness.

At the Outcome level, the following indicators and targets are proposed for use to measure performance;

- Growth indicator – Percentage share of MVA to GDP Increased to 10% by 2025 (up from 7.85% in 2018);

- Competitiveness indicator – MVA Exports per capita increased to US$60 by 2025 (up from US$48.82 in 2017); UNIDO’s Industrial Competitiveness Index (ICI) can be used as a potential outcome indicator. A target rank of below 100, i.e. 90 by 2025 is potentially feasible. Further work could be undertaken led by the Competitiveness Commission to refine this indicator and targets for 2025.

- In addition, GoZ could track on an individual basis – top 5 Manufacturing subsector value added to total manufacturing exports; to include Base Metals; Beverages & Tobacco, etc.

- Inclusivity indicator – Percentage share Manufacturing sector employment to total employment doubled to 8% by 2025 (up from 4% in 2018). This indicator should also be gendered;

- Sustainability Indicator- Emission Intensity (Carbon dioxide emission per unit of MVA in kgCO2 maintained at 0.85kgCO2: 2012). Further studies or input from the Climate Department of the Ministry of Environment, Tourism and Hospitality Industry working closely with the private sector (i.e. BCSDZ) could be used to come up with a refined indicator and target for 2025.

Output level indicators could include the following:

- Total number of manufacturing units/firms categorized by ISIC revision 3 subsectors operating, total number of manufactured products, their contribution to MVA. A baseline survey need to be undertaken to reveal the current status (2020) and come up with a specific indicator and target for 2025

- Total number of manufactured exports categorised by subsectors with RCA of greater than 1. UNCTDASTA Trade Matrix Data Centre of 2018 indicate that Zimbabwe had 10 products with an RCA >1. The target could potentially be set at 15 products by 2025. Further studies involving the Competitiveness Commission could refine this indicator and target for 2025.

- Total number of formal employees employed in manufacturing sectors categorized by ISIC revision 3 subsectors. In addition this output indicator needs to be gendered. A survey is required to establish a base line and targets for 2025.

- Total number of manufacturing firms implementing sustainability programs and number of new or upgraded manufacturing products or services with technical and biological circularity features. A survey undertaken as a component of the Green Industry Program and led by BCSDZ, is essential to establish the baseline and targets for 2025.

The above recommendations and those identified its Zimbabwe National Industrial Development Program (ZNIDP) 2019 -2023 and Zimbabwe- UNIDO Country Program for Inclusive and Sustainable Industrial Development 2016 – 2021 (CP 4 ISID) are key to strategically and systematically unlock the manufacturing sector’s potential in sustaining and creating formal Jobs, enhancing MVA export revenues and attracting much needed technologies and MVA investments. In addition there is a clarion call to all key stakeholders in Zimbabwe, (Government, the private sector, the academia, organized labour, consumers, development partners/donors and IFIs) to work together and make an effort to make the manufacturing sector and the broader ISID, the engine of growth and competitiveness so as to achieve objectives of the Zimbabwe’s National Development Strategy 2021 – 2025 and Vison 2030.

Short term activities

Manufacturing sector short term needs include activities required to set the sector on a firm growth path after two to three years. The sector needs to be restructured, empowered and appropriately funded so as to respond any external challenges it may face. In response to COVID 19 pandemic, the following activities could be undertaken;

- a rapid survey on the impact of COVID 19 on Industry to inform adjustments required in implementation of the ZNIDP 2019-2023 and responses for Thematic Result 5 of NDS, (US$50,000);

- project to assess feasibility of boosting local manufacturer of COVID 19 medicines and medical supplies through a revised Pharmaceutical Strategy 2019 -2023, (US$5m)

- project targeting urban SMEs clothing and leather manufacturing businesses (5,000) in natural clusters to sustain jobs and enhance productivity, (US$5m); and

- UNIDO COVID 19 Industrial Recovery Program (CIRP) to guide appropriate manufacturing sector recovery strategies and activities, (US$2m)

Under the leadership of Ministry of Industry and Commerce, there is need to, among other things, establish a Private Public Partnership (PPP) Industrial Intelligence Unit (IIU) or framework to make it feasible to leverage donor resources for implementation of the industrialization agenda. The IIU is best established as a specific activity under CIRP project with different manufacturing subsectors expected to play a pivotal role in pushing forward sectoral interests. Below are potential projects and programs which could be undertaken during the growth phase of the TWG 5;

- capacity building of the national statistical systems to produce quality and timely Industrial Statistics and Industrial Intelligence, (US$2,5m);

- structured and systematic capacity building for the Industrial Intelligence Unit/system to include selected departments of economic ministries, business associations, public sector organizations, the academia and research institutions through programs such as EQUIP, COMFAR, etc. (US$2,5m);

- project to systematically integrate Science Technology and Innovation (STI) into Zimbabwe’s ISID agenda. This project could focus on building synergies and collaboration between selected Ministries (MIC, MHTEST, MOFED, MOARD, SIRDC, etc.) and between Government and key ISID stakeholders. Issues to be jointly explored would include R&D, Industry 4.0, Digitalization and Innovation, (US$3m)

- Industrial Value Chain Project under which 5 key anchor VC with highest and quick potential to create MVA jobs, exports and investments would be selected, diagnosed and supported (through structured TA and public/private investments, (US$3m);

- project to undertake assessment, re-organize and capacitate ISID financing mechanisms focusing on IDC, Public sector procurement, Buy Zimbabwe and fiscal incentives and penalties, (US$3m)

Medium term outputs/activities

The tail end activities of the NDS 2021-2025 would focus on enhancing further manufacturing sector growth and set a firm foundation to address manufacturing sector competitiveness agenda. These activities assume that most short term activities /outputs were achieved in a systematic, inclusive and sustainable manner. Key medium term activities could include;

- Public sector support through the Annual National Budget (PSIP) or related allocations for Implementation of business/investment plans of the 5 anchor Industrial VCs, (US$2,5m); This is will show Government commitment and ownership of the project and be an essential signal to potential local and foreign investors.

- Public sector investment enhancement for IDC and IDBZ to leverage private sector investments/IFIs facilities, (US$3m); This will also show Government commitment, ownership and serve as a pro industrial growth signal to investors.

- Survey on infrastructure/capabilities gaps for ISID (energy, water, transport, markets, R&D, IT & connectivity), (US$500,000);

- Technical Quality Infrastructure System upgrade and revitalization project (standardization, metrology & calibration, accreditation, conformity/testing & inspection, consumer protection, etc.), (US$5m)

- Buy Zimbabwe and ‘Made in Zimbabwe’ brand project, (US$3m) ; These are great market based strategies to boost local production, sustain and create local formal sector jobs

- Zimbabwe Industrial Competitiveness Project (US$1m); Result of this project would feed into UNIDO’s biannual Industrial Competitiveness Index. The next issue is expected to be published in 2021. This project will also be used to capacitate the recently established Competitiveness Commission so that they learn by doing.

- Zimbabwe Industrial and technology parks project ( to support the transition from low tech manufacturing products to medium and high tech products[xv], (US$4m)

- The Green Industry Program (in the context of Circular Economy – CE) and with funding from GoZ, GEF/GCF and other green funding sources, (US$15m).

Potential funding sources

Zimbabwe will have to rely on its public sector and local resources to support the above mentioned projects and programs. Historically, domestic resources or investments have driven the initial process of industrialization with FDI later coming in when economic growth is firmly rooted in the country. Zimbabwe needs to systematically identify, cultivate and leverage in support of the economic agenda within the NDS 2021 – 2025 and Vison 2030 to include the following donors:

- The EU (under its 2021-2027 funding framework)

- Government of Japan

- Government of South Korea

- Government of Sweden

- United Kingdom

- China

- GEF/GCF

- AFDB/AFREXIM/DBSA, etc.

Section 5: Conclusion

Government of Zimbabwe, the Ministry of Industry & Commerce as the lead Ministry for the TWG 5 ‘Moving the economy up the Value Chain and Structural Transformation’, private sector bodies especially those representing the manufacturing sector (industry) and the academia, are strongly encouraged to make use of this Manufacturing Sector Technical Note as they develop and implement the National Development Strategy 2021 -2025 and beyond. This note has greatly benefitted from UNIDO’s competency as (i) the United Nations specialized agency for supporting the Inclusive and Sustainable Industrial Development (ISID) agenda, (ii) as lead UN implanting agency for SDG9 and (iii) UN agency with global experience and linkages in successfully supporting the Industrialization agenda to include INDUSTRY 4.0.

[i] Generally manufacturing is used interchangeably with industrialization because of the dominance of manufacturing in processing and value addition activities.

[ii] Rama Shankar Pandey, 2020.

[iii] Oxford Business Group, 2020.

[iv] The Pharmaceutical Medicines and Medical Supplies subsector did not record any gains. Most Governments, including those in selected developing countries took advantage of increased effective demand for COVID 19 related medicines and medical supplies to boost local production.

[v] MVA is the total estimate of the net output of all local manufacturing activity units obtained by adding all outputs and subtracting the intermediate inputs. In simple terms it is the difference between the price of product and the cost of producing it.

[vi] ‘Structuralist school of thought’ view development not simply as economic growth but as a transformation of the economy’s structures. In simple terms, structural transformation is a change in the composition of the economy (traditionally divided between primary sector, i.e. mining and agriculture, the secondary sector, i.e. industry, and tertiary sector, services.

[vii] While the three indicators should be interpreted together, the country diagnostic should also highlight differences in the performance of the indicators, e.g. when a country has a large manufacturing sector (MVA/GDP and MVA/capita) but performs comparably poorer in terms of exports (manufacturing exports per capita)

[viii] Higher total employment in manufacturing can generally be interpreted as implying that the manufacturing plays an important role and that it has a higher multiplier effect for job creation compared to Mining and agriculture. Countries which largely depend on extraction and processing of natural resources may have a large share of MVA in GDP, but comparably low employment figures confirm that only a small proportion of the population actually benefits from profits generated by these activities.

[ix] Emission intensity reflects changes in the average carbon intensity of the energy mix used in the manufacturing sector’s structure, in the energy efficiency of each subsector’s production technologies and in economic value of the various outputs. Emission intensity can be regarded as the inversion of emission efficiency, i.e. the lower a country’s emission intensity, the better its performance on this indicator.

[x] Notably subsistence and subsidised agriculture in Zimbabwe

[xi] New and or expansion investments undertaken by Coca-Cola, Schweppes Holding, Pepsi- cola, Commonwealth Development Corporation, several oil pressing companies, etc.

[xii] The concept revealed comparative advantage (RCA) is key when analysing a country’s competitiveness. A country is said to have a revealed comparative advantage in a given product when the country’s ratio of exports of this particular product to its total exports of all products exceed the same ratio for the world as a whole. When a country has a RCA for given product of RCA>1, it is inferred to be a comparative producer and exporter of that product relative to a country producing and exporting that good at or below the world average. The higher the value of a country’s RCA for a given product or industry, the higher its export strength in this product or industry.

[xiii] This potential competitiveness strategy should not ignore other key Industrial strategies to stop further decline of the sector, and support inclusive and sustainable recovery and growth of the industry. Therefore there may be need reconsider renaming the Thematic Working Group 5 to reflect much needed efforts for Industrial Recovery, Growth and Competitiveness.

[xiv] Defined as having GNI (GDP) per capita of between US$3,958 – US$12,235 in 2018

[xv] Premature de-industrialization has also negated the industry’s technological capabilities and innovation.